Making Real-Time Payments a Reality for Finance and Treasury

Real-time payments initiatives are proliferating all over the globe and while many countries have jumped on the bandwagon with various real-time payments use cases, corporate adoption has lagged. But to build the business case for implementing real- time, treasury and finance departments need to identify more business relevant use cases.

How Do Real-Time Payments Work?

Real-time payments can be transferred using the domestic or regional real-time payment network. For example, use an application programming interface (API) for unitary payments like one-time supplier payments, or use file transfer protocol (FTP) for bulk payments like payroll.

While legacy file transfer protocols do not offer the same level of immediacy as APIs, corporates can still benefit from using real-time payment rails in some scenarios.

Moreover, because APIs enable broader system-to- system interactions to be real-time, clients can use them for activities beyond real-time payments, such as connecting to ERPs, automating workflows, and facilitating data exchange in real-time.

Real-Time Systems on the Rise

Real-time or instant payments are not new. Many major economies have either launched real-time initiatives already or are in the process of doing so. For instance, Japan launched the Zengin real-time gross settlement system in 1973, which eventually became a real-time payments network.

- The Unified Payment Interface (UPI) in India, launched in 2016, is among the largest and fastest growing real-time payment system globally. As of 2021, real-time payments represent a 31% share by transaction volume and an 8% share by value.

- Zelle, a real-time payments network owned by seven of the largest banks in the United States, was initially launched in 2017 for peer-to-peer (P2P) payments to compete with payment apps, such as Venmo. Since its launch, this multi-rail network has expanded into business payments and is increasingly preferred by industry use cases, such as real-time disbursements to their customers. In 2021, Zelle added TCH’s RTP® network to its existing list of payment networks, i.e., ACH, Visa Direct, and Mastercard MoneySend.

- SEPA Instant Credit Transfer (SCT Inst), a pan-European payment solution launched in 2017, is used by consumers and businesses for euro-dominated instant domestic and cross-border payments. As of 2022, the payment scheme is supported by 61% of European PSPs and available in 29 countries. The adoption of this payment scheme has stagnated, accounting for just over 1 in 10 credit transfers in the region. A draft EU law is expected to address issues with ubiquity and fees to drive adoption.

- The New Payments Platform There have been ongoing efforts to expand the reach of real-time payments from domestic to cross- border payments. Asia has been leading the way, with India and Singapore linking their real-time payment systems (i.e., UPI and PayNow). Other developed countries are following their lead, with TCH, EBA Clearing, and SWIFT planning to commercialize their successful cross-border pilot connecting TCH’s RTP network with EBA Clearing’s RT1 network.

U.S. Faster Payments Initiative

Unlike many other economies whose central banks have issued mandates for real-time systems, the U.S. Federal Reserve instead opted to let the private sector take the reins while acting in an advisory capacity. Thus, in 2015, the Fed formed a task force of market participants, from banks to corporates to fintechs, with the goal of steering the nation’s payments system toward allowing payments to clear and settle faster. The task force’s work produced a two-part final report that determined ubiquitous receipt to be the key to making any real-time system truly successful. The task force recognized several key challenges to achieving ubiquity, including:

- Federal Reserve enablement of a 24/7/365 settlement

- Technical and business process issues

- Disparate rules and functionality for competing services

- Security

Real-Time Payments Network (RTP®)

In 2017, The Clearing House (TCH) launched the Real-Time Payments (RTP®) network. Running on a new payments rail, Real-Time Payments transactions clear and settle in seconds, and immediate confirmation notices are sent to payers.

In March 2021, TCH announced that real-time payments had reached a milestone by connecting its 100th bank. As of November 2022, there are 280+ participants, plus the key technology providers. However, real-time payments still reach only 65 percent of demand deposit accounts (DDAs).

MAKING HISTORY

The Real-Time Payments (RTP®) network is the first new payment rail in the United States since the ACH.

The Real-Time Payments (RTP®) network is the first new payment rail in the United States since the ACH.

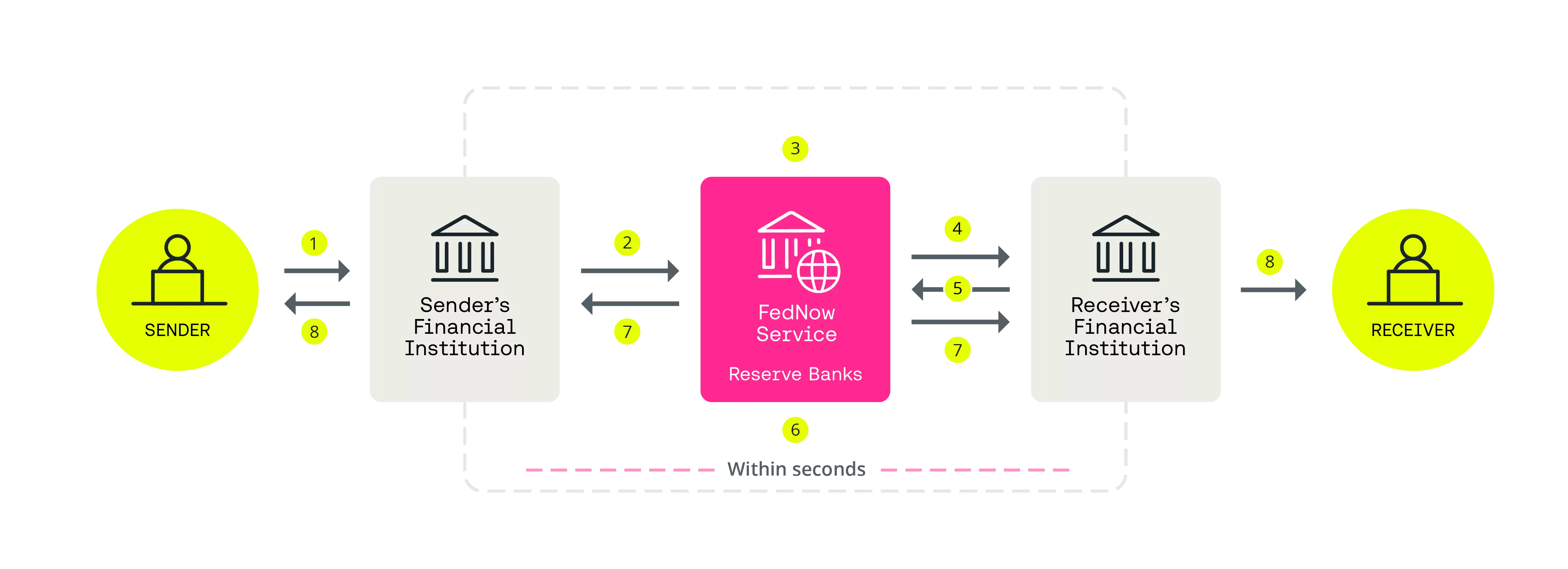

FedNow

The FedNow Service is a real-time payments platform developed by the Federal Reserve as a public sector alternative to The Clearing House’s (TCH) RTP®. The service is a 24/7/365 instant payments network expected to launch in mid-2023.

FedNow will use ISO 20022 messaging standards to enable instant account-to-account payments and be accessible through the upgraded FedLine network, which will enable sending and receiving messages for customer transfers, liquidity management transfers, transaction-level reporting and fraud mitigation tools.

The standard is highly appealing to corporate treasury and finance, because messages carry substantial information and are based on a common data dictionary that supports payment message flows.

INFORMATION > SPEED?

The most appealing feature of both Real-Time Payments and FedNow for treasury and finance might not be speed, but information capabilities. Not only can payers send extended remittance information with payments, but these systems also feature Request for Pay (RFP) services that allow payees to send specific transaction details prior to payments.

The most appealing feature of both Real-Time Payments and FedNow for treasury and finance might not be speed, but information capabilities. Not only can payers send extended remittance information with payments, but these systems also feature Request for Pay (RFP) services that allow payees to send specific transaction details prior to payments.

Corporate Pain Points and Building Real-time Payments Use Cases

For mass corporate adoption to occur, real-time payment systems will need to address certain pain points that treasury and finance departments are looking to eliminate.

| PAIN POINT | HOW REAL-TIME HELPS |

| Emergency/Last-Minute Payments | Particularly in times of crisis like the COVID-19 pandemic, companies may need to make emergency payouts for payroll and other demands. Last-minute bill payments may also be needed. |

| Lack of Cash Visibility | Clearing payments in real-time reduces settlement risk and provides a clear liquidity picture. |

| Need for Cash Conversion | Incoming payments can be immediately turned into accessible cash. |

| Paper Check Usage | Checks continue to be the payment method most susceptible to fraud. Businesses can eliminate this slow and risky method with real-time. |

| Batch Payments | Real-time can “un-batch” payments for corporates. Rather than relying on batch payments that are locked in at key times each day, real-time payments can be sent at any time. |

| Missing Out on Early Payment Discounts | Real-time can ensure that businesses can obtain early payment discounts on the last day of discount availability. |

| Lack of Extended Remittance Information | Modern real-time systems contain extended remittance information that travels with the payment. |

Looking to the future, the U.S. Faster Payments Council identified some real-time payments use cases that could soon make such payments even more appealing:

- Intercompany payments are low risk and a common use case. Many companies have enabled efficient deployment of working capital across their subsidiaries using the domestic/ regional instant payment option.

- Just-in-time invoice payments benefit both the business payer and the business recipient. Since this type of payment gives the payer additional time to pay a bill, it lets the payer hold their funds longer to avoid paying a bill late due to current timing of business day clearing. The business recipient also benefits by ensuring funds are collected within their timeframe, and they receive immediate credit for funds when being paid.

- Payments to suppliers can occur immediately and facilitate faster release and shipment of supplies from suppliers that require payment beforehand. Faster payments involve many moving parts related to treasury functions, remittances, corporate banking, and/or company-to-company payments.

All of these real-time payments use cases involve the movement of large amounts of funds and any reduction in latency will lead to more efficient capital management and reduction of risk. These use cases need standardization and interoperability, such as the efforts of the Business Payments Coalition standardized semantic data model which is being designed to enable comprehensive use case integration in corporate ERP systems.

At ION, there were times when we needed a payment to come in and it was 4:31 and the Fedwire closed at 4:30. We would have to wait until the next day and it would really impact payroll and liquidity. So, the opportunity to have that cash in the bank, and then being able to make your payroll or anything that’s urgent, is where the benefits come in.”

— Lee-Ann Perkins, CTP, Assistant Treasurer, Specialized Bicycle Components and former VP and Treasurer for Ion Geophysical

Key Considerations for Starting your Real-Time Payments Journey

While instant payments have been available for corporates for several years now, uptake has been slow. One reason for that is real-time payments co-exist with wires and ACH. There is still a place for wires, which will continue to be used for larger value payments. As well, the benefits of real- time payments may not justify the cost of shifting to new payment rails. Key reasons for the slow adoption of real-time payments are further discussed below.

Having a small delay when making B2B payments is not necessarily bad.

“There are advantages to it, in trying to plan my cash,” said Jeff Johnson, CTP, chief financial officer of commercial kitchen repair service Smart Care Equipment Solutions. “There are advantages to it if people make mistakes. And there are advantages to not having things rushed.”

Real-time can be costly.

While Real-Time Payments can be relatively costly compared to ACH, they are still cheaper than wires for qualifying volumes. Still, CFOs and treasurers may focus on

the premiums banks charge for Real- Time Payments and not see the value in spending extra cash to ensure a payment arrives faster than a normal ACH, noted Jim Gilligan, former assistant treasurer for Kansas City, and currently senior vice president of MFR Securities.

Real-time may not be exactly real-time on the receiving side.

If the process leading up to the payment execution is slow and manual, then real- time payments won’t have much impact. “Many companies still use batch systems

to process receivables, so payments are not captured real-time,” said Gilligan. “It’s still going to take them the same amount of time to process the payment. Customers will likely be unsatisfied when they realize payments sent in real-time aren’t processed in real-time.” Fintech payment platforms can help bridge the gap by digitizing and automating payment workflows.

Faster payments can mean faster fraud.

Despite awareness of modern fraud activity, treasury and AP departments still fall prey to payments fraud scams even when they have adequate time to claw back a payment. Removing that aspect means that once a payment is out the door, it is gone for good. Bank account verification is key to preventing fraud, and confirmation of the payee is becoming the norm in the context of real-time payments, e.g, in the U.K., 90% of faster payments are subject to confirmation of payee (CoP) checks.

It’s clear businesses need to be more thorough in vetting payments before they are executed. While it’s unrealistic for an organization that remits hundreds of payments in a single payment run to manually check every single one, technology can help to eliminate the threat.

- Payment policies can be digitized, ensuring that rules and limits are automatically applied during the payment journey.

- Artificial intelligence (AI) and machine learning (ML) algorithms can compare outgoing payment requests to historical payment patterns, identifying and isolating any anomalies.

- APIs built into your payments platform allow real-time connection to apps that can match payments against third-party data. This data allows you to verify ownership of the account you’re paying and that you’re not paying an entity on the Office of Foreign Assets Control (OFAC) sanctions list.

- Data visualization can identify and manage exceptions so that payments can easily be reviewed and cleared to minimize delays.

Technology has really come a long way. Number one, there’s a lot more data to pull from that makes the software that much smarter. Number two, there’s a lot more threat intelligence available, and an increasing element of collaboration and sharing that threat intelligence. Today, you can run a transaction through an enormous number of tests in less than the time it takes to blink an eye. It adds a real element of credibility to a transaction.”

— Brad Deflin, Founder and President of Total Digital Security

How to Start Building Your Real-Time Payments Use Cases

For U.S. corporate treasury departments that are interested in real-time payments, they will first need to develop their own adoption strategy:

- Determine some key uses cases for your business. Your bank and/or provider can offer live examples to help you narrow down use cases, understand the benefits, and calculate the business case.

- Assess the risks that using a new, real-time payments rail could pose, such as the need to update payment governance procedures to prevent fraud.

- Engage banks and vendors to ensure that they have invested in the appropriate infrastructure to facilitate real-time payments.

Real Opportunity

Real-time payments present an opportunity for corporate treasury and finance departments.

Corporates that manage their own bank connectivity may need more work to identify use cases and build a business case for investment. For corporates that rely on third-party providers to aggregate connectivity, common real-time payments use cases such as sending intercompany transfers or replacing wires at or under the current transaction limit can drive tangible value while the corporates explore broader use cases.

Watch this on-demand webinar to learn more about how you can build compelling real-time payments use cases in 2023 to benefit from this payment type.

Learn more about real-time payments in 2023 in this webinar

Success Story