Open banking is a banking practice that gives consumers full control over their own banking or financial data so that they can decide whether any third-party financial service providers can access the data to provide them with better products and services. That’s why it is also known as "open bank data”.

Open banking is enabled by the use of APIs. In Europe, the legislation of PSD2 (Payment Service Providers Directive) has been a main driving force behind making open banking a reality for every consumer.

Open banking has also become a hot topic for corporate treasurers because many of the Open banking use cases and their associated benefits are applicable in the business context too, especially when it comes to system integration and real-time data accessibility.

What Are the Main Purposes of Open Banking?

Open banking is a step forward in the future digitalization of financial services. When people ask why open banking, consider the following two main areas open banking will drive positive changes:

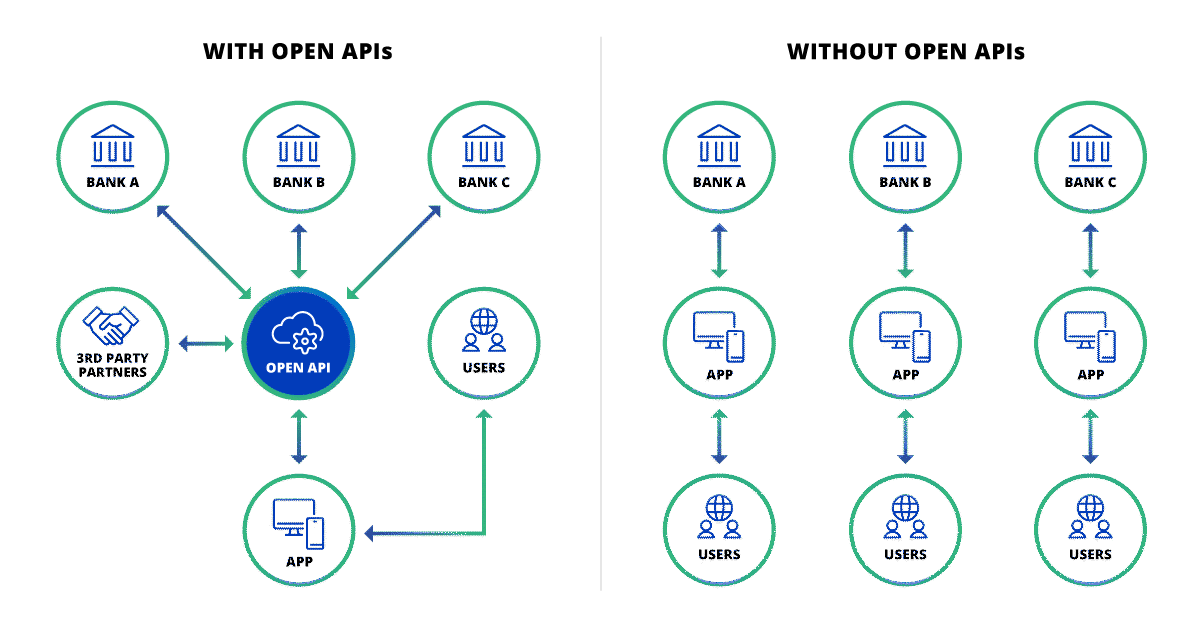

- Open innovation. Banks have always been like walled gardens. If you have two bank accounts at two different banks, most likely you have to log into two banking apps to manage your money. It is so for security reasons, but it also creates inefficiency. Now with consumer’s consent, Fintech startups can gain access to consumer data at any bank through Open API. This has boosted innovation in the financial services industry.

- Service customization or personalization. When consumers are no longer tied up with one bank’s own designed products and services but a whole ecosystem of apps, there is a lot of space for customization or personalization. For example, when you give your consent, third-party apps can use your banking data to offer products and services that are tailored to your financial situations.

Is Open Banking Secure?

It is unsettling for many people when they hear that their banking data will be shared. This is a well justified concern. There is always some associated risk when data is handled online. However, open banking security has been deeply designed into the processes and legislators in different countries are watching this space closely. For example in Europe consumers have improved security with PSD2’s implementation of Strong Consumer Authentication (SCA).

Two things are important to keep in mind for open banking data sharing. First, without your consent, your banking data cannot be shared by your bank or any third party service provider. Afterwards, you also have the right to ‘unsubscribe’ any time from the data sharing. Second, even with your consent, you will not share any credentials such as log-in username or passwords. The data to be shared usually are things like type of the account, name of the account, transaction history, or balance details.

What Are the Benefits of Open Banking?

For consumers, the main benefits of open banking are:

- Full control of their own financial data

- Enhanced banking experience across different financial services

- Reduced costs with much lower switching costs

- Quick access to the latest and greatest Fintech innovations

For corporate treasury, the main benefits of open banking are:

- KYC process can be streamlined with API integrations

- Quick access to and adoption of the latest and greatest Fintech innovations that are targeted at corporate financial challenges

- Real-time treasury becomes possible with the proliferation of faster payments, instant settlement, and real-time availability of balance and transaction data

Use Cases of Open Banking for Corporate Treasury

The following open banking use cases are often discussed in different treasury forums and can be a good starting point for corporate treasurers to consider:

- Real-time cash visibility: API connectivity aggregates in real time the cash position into any system of your choice–for example, it can be your TMS system or your ERP system–to make available figures from all bank accounts into one centralized view for unprecedented instant cash visibility. In practice, this means that the time and effort of logging into multiple banking portals or systems to download and consolidate the bank statements and transaction data can be saved. This also means that the cut-off time for intraday statements will no longer be the bottleneck of data reconciliation, as data arrives at your system of choice instantly.

- Inbound and outbound payments: API-based real-time payments can bring tangible benefits to corporate cash management because it transforms the current payment processes both in terms of speed and tracking of both inbound and outbound payments. Treasurers choosing to adopt the new world of instant payments have already seen concrete business outcomes. For example, Kyriba client Hunt Companies gained both cost saving and efficiency by being an early adopter of ACH’s RTP® network in the USA, reducing its bank fees from $6 on average for a wire transfer to less than $1 for RTP.

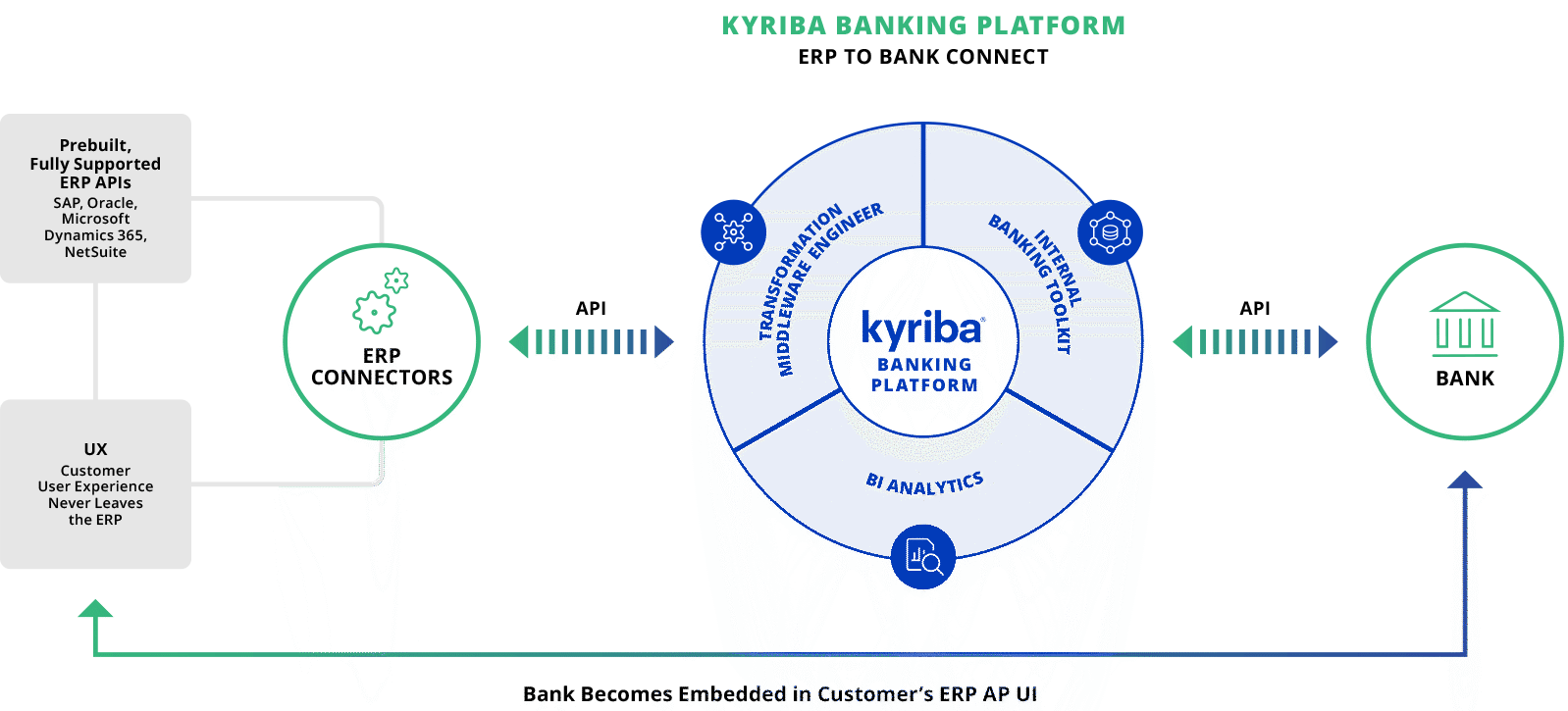

- Data aggregation for real-time decision making: Data is the real link behind various processes within an organization and poses opportunities to form cross-functional business optimization. For example, traditional FTP connectivity between TMS and enterprise resource planning (ERP) systems is being replaced by API for data exchange (e.g. Kyriba provides API-based ERP connectors for SAP, Oracle, D365 and Netsuite). Accurate real-time data enables better decision-making, including timely analysis and forecasts, and mitigation of financial risks. On top of that, when data becomes available in real-time, there is a new opportunity to apply other technological enablers to use the data to achieve new levels of cash and liquidity management. The use of artificial intelligence (AI) for example to automate cash flow forecasting has been gaining its ground among corporate treasurers.

The possibilities with APIs are infinite. Check out more use cases enabled by Kyriba’s Open API platform and see how they can support your organization to bring your treasury, cash, payments and working capital to the next level.

Challenges with Open Banking for Corporates

Despite the promising future of open banking for both consumers and businesses, there are still a few challenges that remain:

- Lack of standardization: APIs are a new addition to the bank connectivity, and each bank has their own way of defining how they transfer data. A universal standard does not exist, which means each time you connect to a bank API, it becomes a project of its own.

- New technology meets old technology: Technology evolves rapidly year to year. Both banks and corporates grow their IT infrastructure over the years with numerous hardware and software additions and upgrades and system migration and updates. When a new tech stack meets the old, things do not work automatically. The idea of using APIs to connect systems for real-time data transfer is great but in reality, the task to make it happen is not to be underestimated.

- Balance of openness, security and data privacy: Concerns over data privacy, security and compliance have grown among legislators, regulators, companies as well as ordinary citizens. Actions are being taken in different parts of the world to ensure a balance between open innovation and data security. For example, in Europe, the General Data Protection Regulation (GDPR) has been published since 2016 to protect against data breaches.

How to Use Connectivity-as-a-Service

There are many ways to start benefiting from open banking.

One good place to start is to look at the current and future needs of connectivity for your treasury operations. No matter what you want to do with open banking, it always starts with the connectivity, whether it is connecting to different banks’ APIs, integrating the products and services from Fintechs, or building data pipelines with strategic business partners for your own data lake.

Due to the importance of APIs for open banking, it is recommended to discuss the API roadmap with your banking partners or system providers to ensure that you have enough visibility into the capabilities they will provide to meet your future business and growth needs. Choosing a technology provider and adopting Connectivity-as-a-Service is a good start for your open banking initiatives.

When to Adopt Open Banking in Treasury

Many companies and treasury teams with limited IT resources are still on the lookout for options to adopt the open banking technology. Due to the nature of the APIs provided by banks and financial institutes, both the number and the specifications are constantly growing and changing, posing challenges to find actual business cases or the IT resources to take them into use.

However, it is important to bear in mind that existing connectivities to your banks, such as SWIFT, EBICS, and H2H, are complementary to APIs so that all data that is not yet made available via APIs can be aggregated by these existing set-ups. Therefore it is already possible for the more advanced treasury teams to begin the journey now and start preparing the set-up for open banking and real-time treasury.

In addition to using existing connectivities, it is important for companies to identify specific use cases where open banking can add value, such as optimizing cash management or improving liquidity forecasting. This can help justify the investment in IT resources and ensure a successful implementation.

Companies should prioritize security and data protection when working with open banking APIs. This includes ensuring that all data transfers are encrypted, using secure authentication methods, and implementing strict access controls.

Finally, it can be helpful to engage with other stakeholders in the industry, such as partners, banks, and fintechs, to share knowledge and best practices. This can also help identify potential collaboration opportunities that could further enhance treasury operations through open banking.